Part I: A recap……This two-part blog opened with a legal triumph, one of the vestiges of global imperial and cold war politics, took a major step towards a solution in October 2024. Aided by the election of a new Labour-led government in the UK in that same year, the UK announced it would finally give up its sovereignty of the Chagos islands, and after years of negotiation, return them to Mauritius. So far, the narrative about the legal case has neglected the possible economic implications for Mauritius, specifically the possibility of a resource curse as a result of the rental-cum-compensation payments for the Diego Garcia military base. The first blog in this two-part series established the reasons Mauritius should be wary of the resource curse, check it out here.

Part two works through the relevance of various mechanisms by which a resource curse could operate in Mauritius. The blog concludes with a big idea how a potential resource curse could be turned into a knowledge-blessing.

The Dutch Disease

The model of the Dutch Disease was inspired by the experience of the Netherlands, which discovered offshore gas deposits in the 1950s and subsequently experienced a decline in their manufacturing sector. As a country begins exporting natural resources, foreigners wishing to buy the export have to purchase the local currency. This causes an appreciation of the local currency which in turn makes other exports (such as manufacturing) less competitive. Another mechanism is that resource wealth may increase the demand for non-traded goods, such as real-estate and haircuts. Think here of oil company executives and oil ministers buying expensive apartments and dining in fancy restaurants. This in turn may pull resources such as land and labour from manufacturing and into the construction and service sectors.

The key policy suggestion is firstly for countries to prevent an appreciation of their domestic currency and secondly, over time to promote a diversification of the economy out of the primary sector. First, a country may prevent its currency from appreciating by increasing the domestic money supply through foreign exchange interventions. To prevent inflation, they may also introduce sterilization policies, such as raising reserve requirements on banks. If the commodity boom proves to be long-lived the country may allow a gradual appreciation of the currency. Second, governments must promote economic diversification during boom periods. For example, when Norway experienced its oil boom, it insisted on joint ventures and trained up petroleum engineers (at the Norwegian Technical University and Rogaland Regional College). The Norwegian industry became expert at producing deepwater drilling platforms. Such efforts do not always work. In Nigeria, the government used oil revenues to promote the manufacturing sector, but this was an inefficient process and the new enterprises were not productive and cost-effective enough to export, remaining dependent on subsidies to survive. When the world oil price declined in the 1980s, the manufacturing sector in Nigeria collapsed.

Institutions as Protection and Institutional Decay

The resource curse literature has found that the negative impacts of resource exports are concentrated in those countries with bad institutions. On the other hand, those countries who have turned a potential resource curse into a resource benefit have included Botswana (diamonds) and Norway (oil), which both had good (producer-friendly) institutions in place at the time the resource was discovered and production began. Better institutions can more effectively engage in targeted monetary policy and allocate windfalls to productive uses. Rigorous statistical evidence shows that institutional quality (measured in relation to variables such as bureaucratic quality and government corruption) can reduce the negative impact of resources on economic growth. Another study finds that in aggregate natural resources have a strong, robust, and negative effect on growth between 1970 and 1998, but once institutions are controlled for, there is either very little effect of natural resources on growth or even a positive effect.

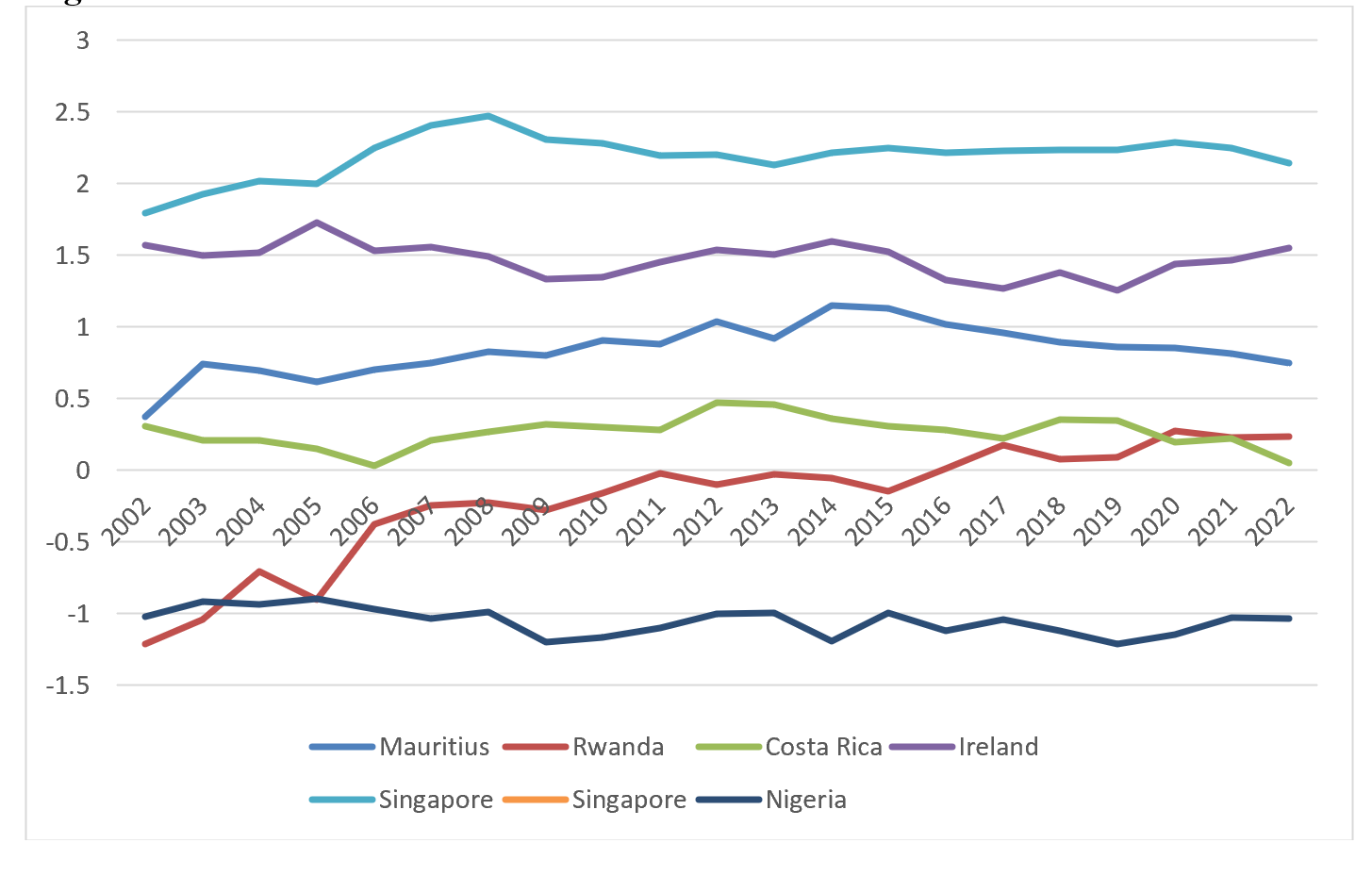

Figure Two shows a measure of government effectiveness from the World Bank for Mauritius and four comparable countries (Ireland, Singapore, Costa Rica, and Rwanda) that are all relatively small in terms of land area and population but which have noted success in attracting FDI and promoting rapid economic growth. The index produces a measure between +2.5 (the best) and -2.5 (the worst) and captures “perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government's commitment to such policies.” Figure Two shows that Mauritius has relatively high-quality institutions, not of the standard in Ireland or Singapore, but good compared to (improving) Rwanda and Costa Rica and much better than Nigeria.

Figure Two: Government Effectiveness in Mauritius, Four Comparator Countries, and Nigeria

Source: World Bank (2024).

Institutions do not just mediate the impact of resources on economic outcomes, they are also directly impacted by resources, high levels of resource revenues often undermine governance quality. For one, resource windfalls reduce the need for states to tax citizens to raise revenue, reducing the need for politicians to invest in building the state’s bureaucratic capacity. Elected politicians may also seek to dismantle well-functioning institutions such as budget transparency and rules governing the use of natural resources, in order to gain access to resource rents. Where resource-funded patronage is an option politicians can instead buy off a larger set of potential challengers and reduce dissent. Resource funded states are freed from the need to levy domestic taxes and become less accountable to the societies they govern. One study finds that fuels and minerals have a systematic and robust negative impact on growth via their negative effect on reducing institutional quality. Another study provided a rigorous test of this hypothesis and found that a sudden surge of revenue to local governments in Norway reduced public sector efficiency, measured in terms of the output of public services (care for the elderly, primary and lower secondary education, day care, welfare benefits, child custody, and primary health care) from a given volume of spending. Importantly for this discussion of Mauritius, the evidence shows that natural resource revenue has the same impact as windfall revenue derived from other sources, such as rents on a military base!

Saving and Investing Resource Windfalls

A key link between the resource curse and economic sustainability is the question of whether the resource revenues are being consumed or saved and invested. Countries receiving resource windfalls, especially those with weak institutions and dysfunctional political systems, have found budgetary prudence difficult to achieve. A study using cross-country data between 1980 and 1995 finds that resource-abundant countries tend to have a negative savings rate (-2.6% of GDP on average), while resource-poor countries often have a positive savings rate (+9.2% of GDP on average). Those countries that have used resource abundance to finance current consumption have experienced slower economic growth. The resource curse is entirely explained in one study by the interaction between resource availability and government consumption.

Investing rather than consuming the proceeds of natural resource wealth is no panacea for economic growth. There is a long history of centralised resource wealth being used to promote inefficient industrial import substitution. In Nigeria, there was a massive surge in investment led by the public sector, most of which was wasted. The most famous example is that of the Ajakouta steel complex, where construction started in 1979 and four decades and hundreds of millions of dollars later, the complex has never produced a commercial ton of steel.

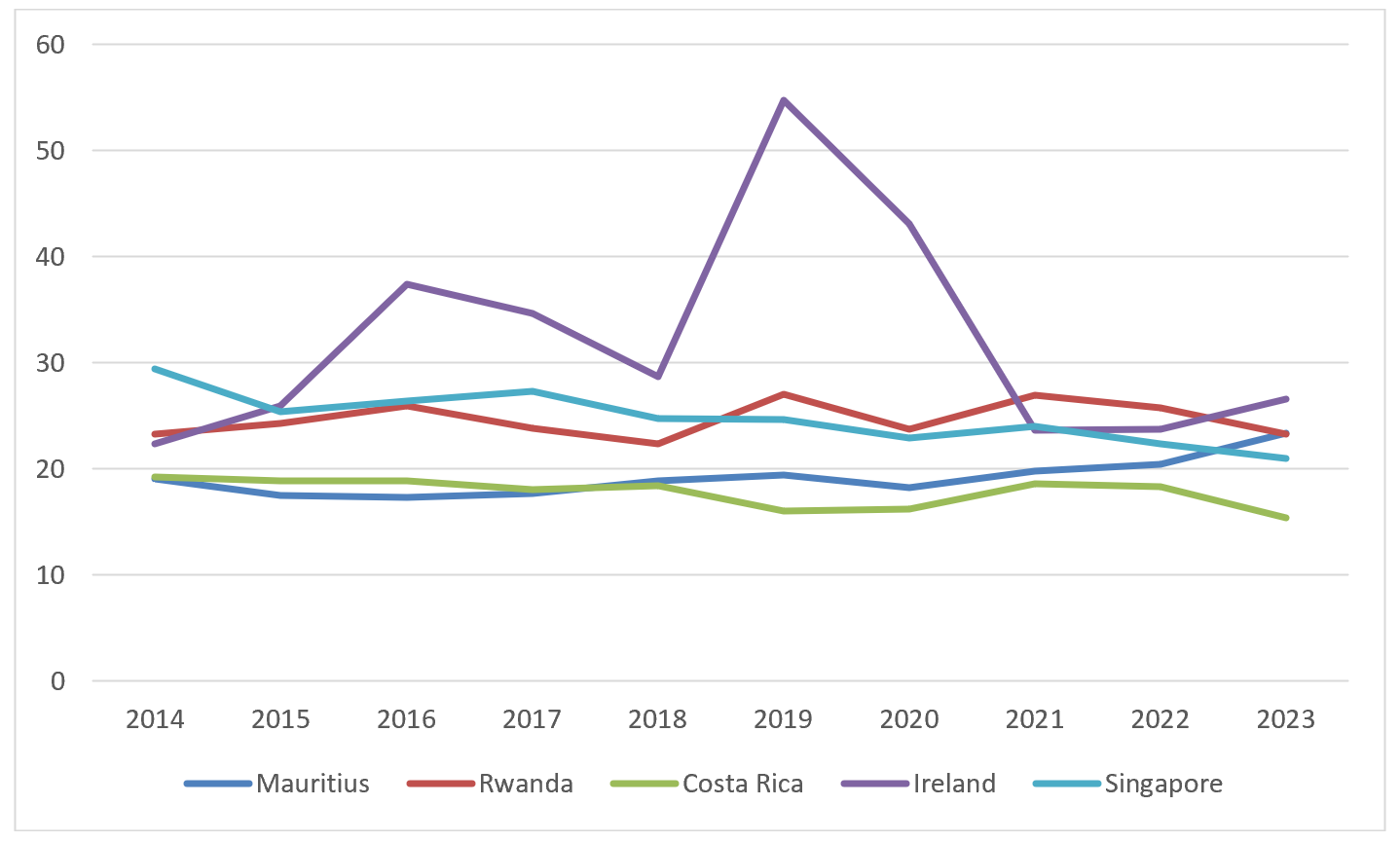

There is no rationale for Mauritius to use the Diego Garcia rent to undertake a massive increase in investment. Figure Three shows that investment in Mauritius is slightly lower, but entirely comparable to the four other successful small countries. Lower income developing countries typically require investment of 30-35% of GDP to sustain rapid economic growth. Mauritius has already built the ports, housing, airports, roads, and factories it needed to sustain textile-led manufacturing export growth between the 1970s and the 1990s. Today, Mauritius, as in the case of Singapore or Ireland, can sustain rapid economic growth in knowledge-intensive service sector with investment around 25% of GDP.

Figure Three: Gross capital formation (% of GDP)

Source: World Bank (2024).

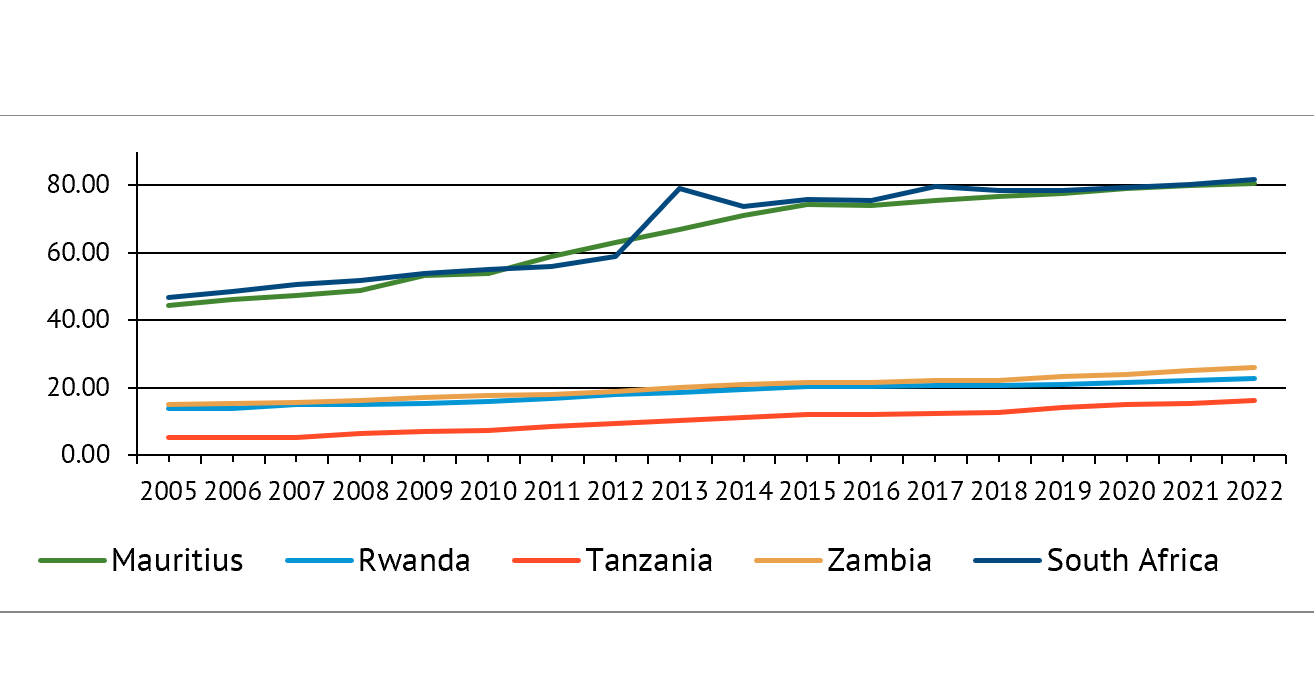

Further evidence of this can be seen in the specific case of infrastructure investment. The Africa Infrastructure Development Index (AIDI) Index covers the period 2000 to 2018 and comprises indicators related to electricity, transport, ICT, and water and sanitation. Figure Four shows that Mauritius has a massive advantage over almost all African countries other than South Africa. The favorable picture diminishes once Mauritius is compared to global standards, but this indicates steady improvements are needed, not a massive investment in infrastructure provision.

Figure Four: Infrastructure in Mauritius and Four African Countries

Private Saving and Foreign Saving

The previous section concluded that Mauritius should save its Diego Garcia rents, but not engage in a state-mediated effort to boost domestic investment. There are two options for Mauritius to fulfil these policy recommendations. The first is to recycle the revenue to the local population and the second is to create a sovereign wealth fund (SWF).

In the US state of Alaska, the Alaska Permanent Fund saves earnings from the state’s oil sector. Alaska state law says the Fund must distribute half of the investment earnings on an equal per capita basis. The motivation is that citizens are better informed about the returns from saving and investment. The system gives Alaskans a position as stakeholders in the Fund. In 2003, one study proposed doing the same in Nigeria and estimated that this would then be equivalent to each adult getting roughly $760, representing about 43% of current per capita GDP and double the US$1 per day poverty line. The main problem with this choice is that it would require converting the dollar rental payments into Mauritian rupees, with all the attendant problems related to the Dutch Disease discussed earlier.

The second option is to create a SWF. By 2015, there were more than 50 global SWFs established using the proceeds of resource revenues, including in Australia, Bolivia, Chile, Gabon, Ghana, Mongolia, and Turkmenistan. In the US, the states of West Virginia and North Dakota have established their own SWFs. Some funds are managed by the existing fiscal authorities and operate within the budget framework without revenues being earmarked for any specific purpose. Other funds are managed by specially appointed boards and operate partly or wholly outside of the government’s budget. Often the revenue derived from formal funds are earmarked for special purposes. The record of SWFs is mixed. Those that have been successful are in democratic or partly democratic countries that are well-functioning, transparent institutions, with a predictable and stable legal framework. The characteristics of a well-functioning SWF include simple and transparent regulations, as well as the public availability of information about the rules, the funds, and the investments. Managers are accountable not only to the government and to the parliament but also to the public, which in itself, generates citizens interest in fund management. While the example of the Norwegian SWF is often used as a global example of good practice, Norway discovered oil when its institutions were already highly developed. Management of the Botswana Pula Fund is perhaps more suitable for Mauritius, where the revenue is managed by independent professionals with instructions to pursue only the financial interests of the people of Botswana and not political goals.

Conclusion and a Big Idea

The big policy conclusion of this policy brief Mauritius can avoid the problem of the Dutch Disease by saving, investing, and diversifying, rather than consuming, the Diego Garcia rental payment through the creation of a SWF. The existing good institutions in Mauritius offer reason for optimism, but concerns still linger due to their steady deterioration over the last decade.

Ultimately, Mauritius needs investment in knowledge creation more than physical factories and infrastructure. As a middle-income country, Mauritius is looking upwards and aspiring to the success of small, but high-income countries like Singapore and Ireland. In one way they are completely different. The leading higher education institute in Mauritius, the University of Mauritius, ranks between 1200-1500 in the Times Higher Education University World

Rankings. Here Mauritius looks more like the University of Rwanda or University of Costa Rica (both ranked outside the global top 1500) and less like Ireland’s Trinity College Dublin (ranked 139th) or the National University of Singapore (ranked 17th). The investments needed to build a world-class university could be made in dollars, payments to foreign-recruited researchers, teachers, and administrators; importation of research materials and laboratory equipment, and scholarships for students. This would minimise the problem of converting dollars into rupees and so with it the problems of the Dutch Disease. Like any domestic budget process, the hiring, functioning, and management of a revamped University of Mauritius should be done within the full glare of transparent procedures, management, and accountability. A resource curse that threatens government institutions or the functioning of democracy could easily transfer its damaging impacts to the confines of a university.

Because of the pivotal elections in the US and Mauritius the Chagos deal has come under renewed scrutiny. The incoming Trump administration concerned about the geopolitical implications and Mauritius with the length of the lease on the military base. These political concerns should not allow Mauritius to get distracted from planning for how to best utilize the rental payments on the military base should the deal finally be agreed upon, there is a danger of a resource curse, but also a real possibility of a resource blessing that could help Mauritius achieve sustainable and knowledge intensive economic growth.

Thanks to Ashwin Roy who originally asked the question ‘could the Chagos ruling create a resource curse for Mauritius’?